Equity 101 for Software Engineers at Big Tech and Startups

A growing number of startups and Big Tech companies offer equity - stocks, options, and others - as part of software engineering compensation. However, I've noticed few engineers understand what these mean.

When I was a hiring manager at Uber in Amsterdam, engineers usually focused far more on the base salary, taking little interest in equity. Several people only realized much later - sometimes at the IPO - how big of a deal a good equity package means.

"Why should I care about equity?" is a question I frequently get, especially from engineers who have yet to be issued equity. Here's why: for almost all total compensation packages over $250K in the US and €150K in Europe, an increasing chunk of it is equity. Both publicly traded companies in Big Tech and startups frequently issue meaningful stock to software engineers.

This post attempts to summarize the most common equity compensation setups you might come across, help you understand their value, and point to additional resources. This is the information I wish I knew earlier to understand how equity works at the high-level, and help me do more detailed research when I got offers that contained equity components.

Disclaimer: this article is not tax or legal advice or advice of any form. Though I have received options, RSUs and been part of ESPP schemes: I'm no financial advisor or expert on the topic. Do your homework beyond this article: read the fine print in offers, talk with people who have more context, or find an expert.

Books that go deeper in the topic - especially for equity with US-based companies - are:

- Equity Compensation for Tech Employees - a book I reviewed, written by Matt Dickenson, software engineer at Square.

- The Holloway Guide to Equity Compensation - a popular book for tech employees.

We'll cover the following topics:

- Why Equity is Important: Success Stories

- Vesting, Cliffs, and Clawbacks

- Stock Options, ESOPs and NSOs

- RSUs (Restricted Stock Units)

- Double-trigger RSUs

- ESPP (Employee Stock Purchase Plans)

- Phantom Shares

- SARs (Stock Appreciation Rights)

- Virtual Shares, Virtual Options

- Growth Shares

- Dilution

- Taxes

- Why Equity is Illusive: Cautionary Examples

1. Why Equity is Important: Success Stories

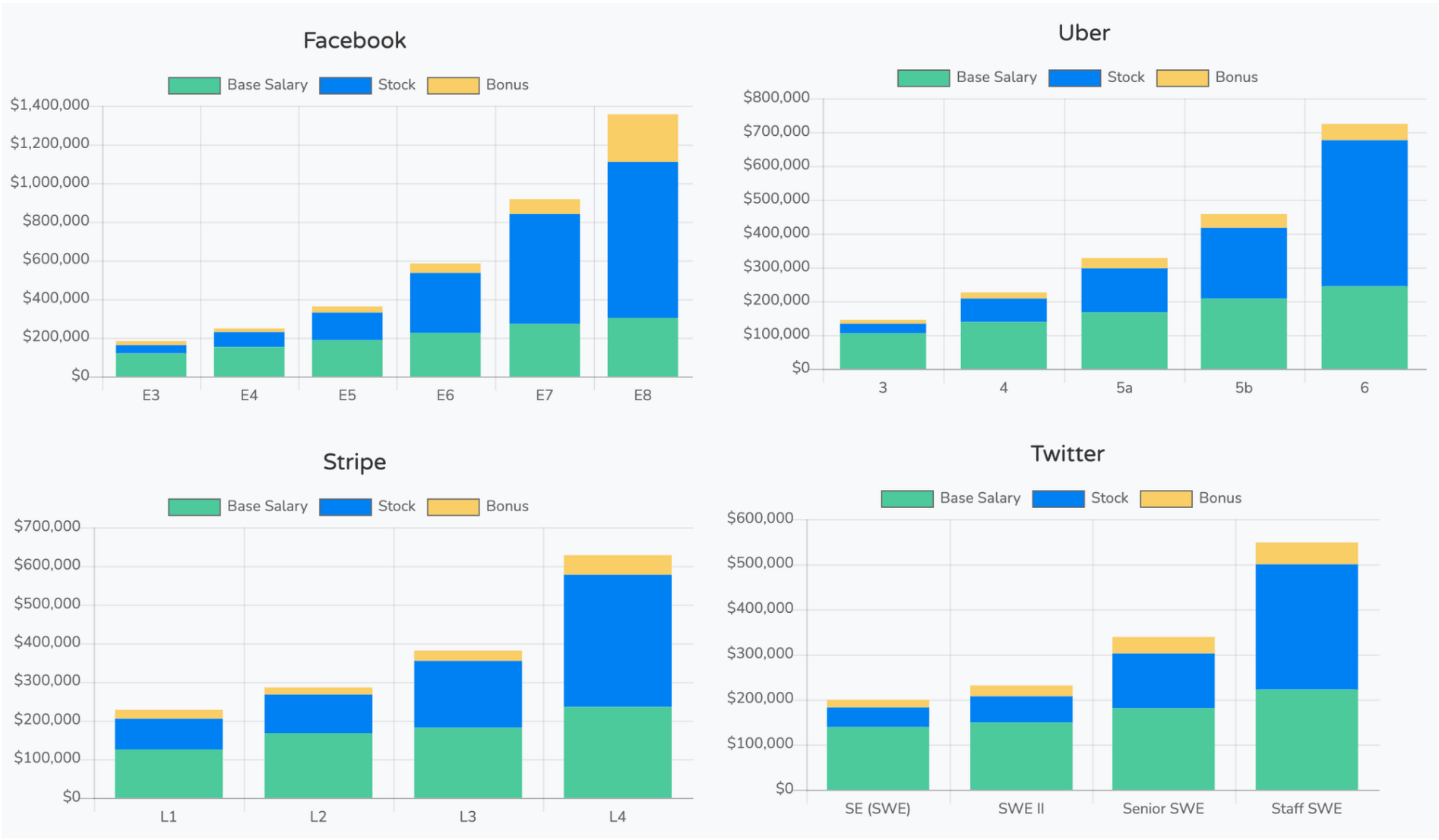

Equity is an important compensation component for software engineers at Big Tech and the "top" tech startups. At places like this, staff and above levels in the US often receive more in stock per year than their base salary:

For the majority of software engineers I know - including myself, based in Europe - equity has been hugely beneficial. Still, few people have heard of these stories from friends and assume equity upsides are limited to either those in Silicon Valley, or to executives.

Here are a few outsized success stories to illustrate the type of gains software engineers have seen in the past:

- $12M in options and stocks gain for a software engineer who joined Doordash in 2018 as a software engineer 2 (source). They were allowed to sell their stock starting May 2021, after the 6-month lockup expired.

- $10M in equity gains for 4 years' of equity vested for the first 10 engineers at Amplitude, an analytics startup (source: the founder). The startup was the first to put extremely employee-friendly equity policies in-place, like a 10-year post-termination exercise window. This meant that even if any of these first 10 employees left after 4 years, they still made $10M or more without having to exercise their options, and could do so, years after, on the IPO.

- $6M in options gains for a software engineer at Databricks who accepted an offer late 2018 that included 50,000 options spread over 4 years (source). Databricks was valued at around $1B at this time - as of February 2021, it is valued at $28B. This engineer has not yet vested all options, and they are not yet liquid - but there's a high chance they will be, following an IPO.

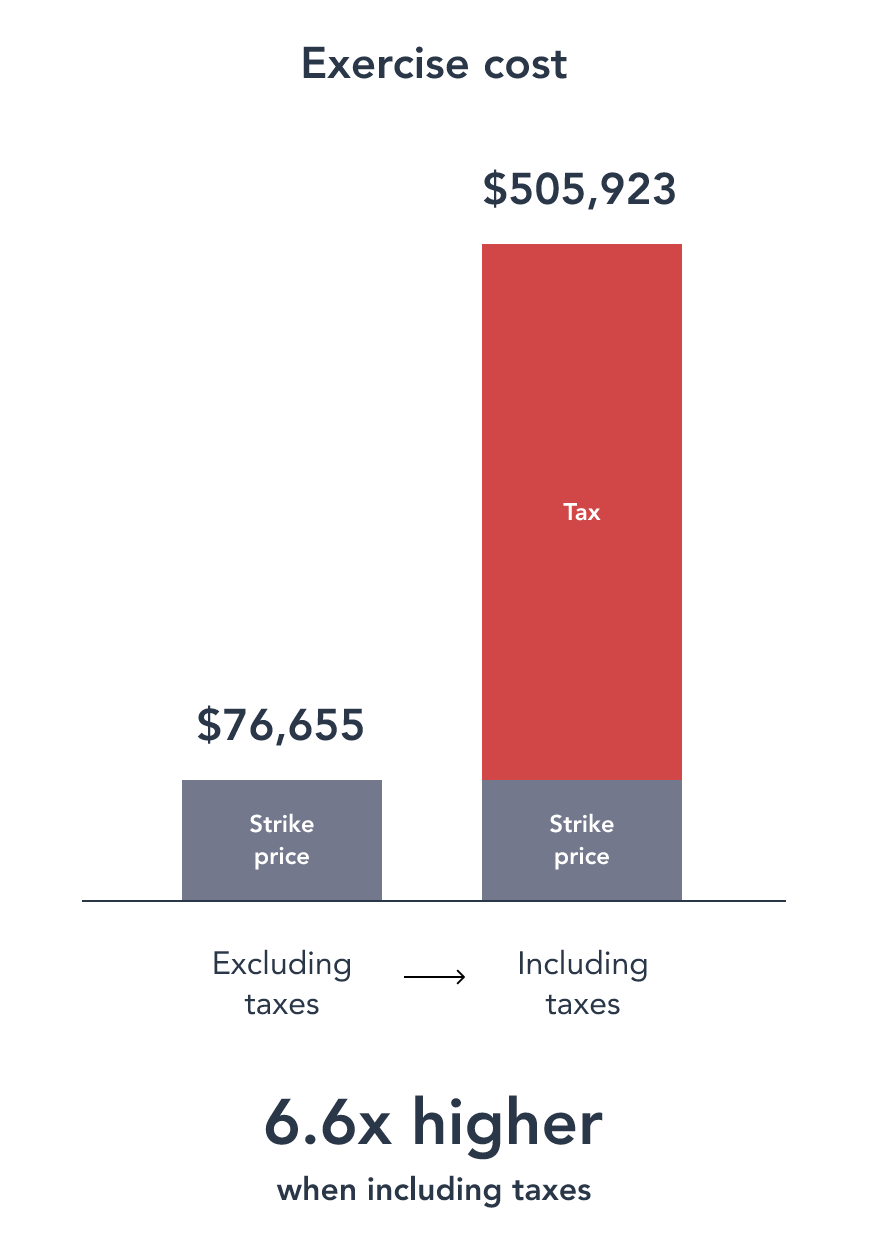

- $2.2M in gains in 1.5 years for a software engineer who joined Snowflake in 2019, 1.5 years before its IPO. Taxes were a big source of this engineer, with the exercise cost and taxes accounting for $508K (the gains were on top of this). Source: Secfi state of tax options 2020.

- $600K/year for a staff software engineer at Google in Washington with the following setup: $240K in base salary, $300K/year in Google stock, and $60K in cash bonus. Staff and above levels making more in RSUs than base salary is not uncommon at publicly traded Big Tech companies in the US.

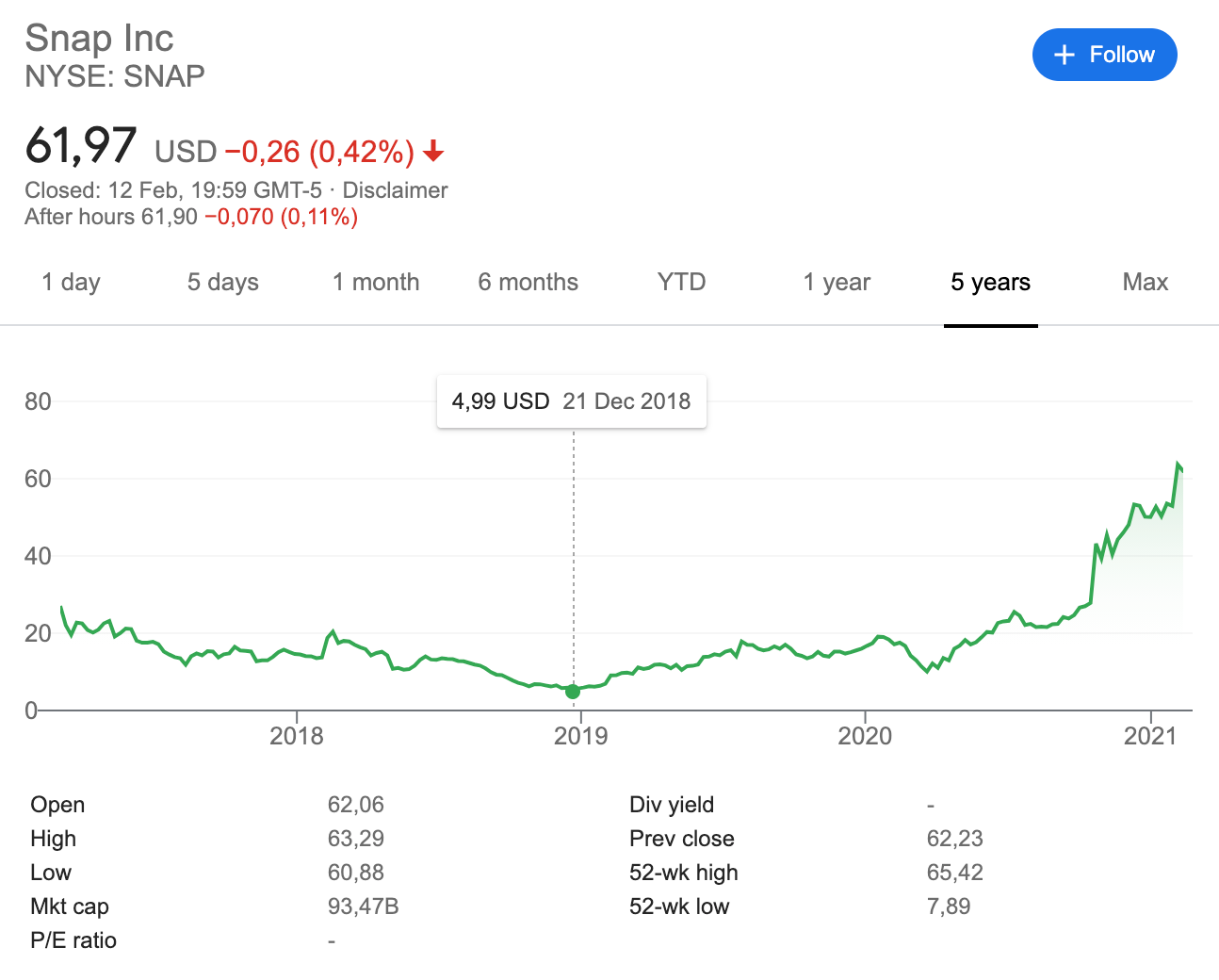

- €500K/year at Snap, in Europe for a senior engineer, thanks to stock rises. A person I know received an offer at Snap with €100K/year in base salary and $100K/year in RSUs. They received RSUs around $10 each in early 2019 - a total of around 30,000 RSUs. The stock has grown by more than 6x, and this person is currently vesting around €400K/year just in stock. Had they not received such a strong equity package, they would not have benefitted from the rise in equity.

- Non-senior software engineer making €250K/year in Germany thanks to equity. A software engineer received 4,000 RSUs vesting over 4 years when joining Airbnb. At the time, the internal stock price was at $60, valuing this package at $60K/year (1,000RSUs/year), on top of their €90K/year salary. Following the IPO and the increase in share price, the equity is worth around $180K/year (at a share price of $180/share and 1,000 shares/year - €150K/year), bringing their total liquid compensation to around €250K (including an annual €10K bonus).

All of the success stories can be attributed to meaningful equity offers and the equity value of the companies skyrocketing. Both Doordash and Databricks have increased their company valuation by more than 30x in the past 2.5 years - and even with dilution, equity holders saw probably 20x or more in gains. Valuations for Snap and Airbnb have risen by 4-6x in the past two years.

Equity, however, is risky. There is no guarantee of an IPO, and even less of the stock jumping as much as it did with Doordash or Airbnb.

This article will close with cautionary stories where people were left with nothing - or - even worse - lost lots of money through options. There is no free lunch, and you will not see outsized gains without taking on some level of risk.

2. Vesting, Cliffs, Refreshers and Clawbacks

Any time you'll be awarded equity, you'll see a few common terms.

Vesting refers to in what installments you'll "get" the equity. Say you are awarded 48 shares - or options - over 4 years, and they vest quarterly. You would get 3 shares - or options - each quarter. If you stay for the full 48 months, all 48 of your shares/options vest.

Cliffs are a clause that requires you to stay at a company for a minimum amount of time before you get any equity. In the previous example, without a cliff, you could decide to quit after 3 months and still walk away with 3 shares/options. This might be in your interest, but the point of equity is to incentivize staying long-term.

A one-year cliff is typical with privately traded companies and is usually not negotiable. Going back to the previous example: 48 shares over 4 years, vesting quarterly, with a 1-year cliff would mean this vesting:

- 3 months, 6 months, 9 months: no shares.

- 12 months: 12 shares

- 15 months: another 3 shares... and the same, every 3 months.

For publicly traded companies, no cliff on vesting is becoming more of the norm in big tech. Google, Facebook, Spotify, Pinterest, Uber and Doordash all issue stock with vesting starting immediately: so you can share stock after the first month or quarter (depending on the vesting schedule).

Conversion from monetary value to shares or options could happen at two timeframes:

- Converting when awarding the grant. This is the most common scenario. For example, if you join Microsoft and your contract states you are awarded $244,000 in stock over 4 years, and Microsoft's stock price is $244 at this time, then you'd get awarded 1,000 units of stock to vest over time. This approach ensures upside if the stock goes up - but also downside if it goes down.

- Converting on vesting of each stock unit. This is an approach Stripe, Lyft, Walmart and a few other companies are taking as of recently. Say you are awarded $480,000 of Lyft stock to vest over 4 years, at a monthly cadence. After the cliff, you'd be allocated $10,000 worth of shares every month, converted on the spot. This approach ensures you get $10,000 worth of stock every month: but you get no upside from the stock going up or see a downside if it goes lower.

Equity refreshers are something that many Big Tech companies award to either a wide population or to people perceived as top performers. They are typically awarded annually and can have a different vesting schedule from your original equity awards.

While I was at Uber, both myself and most people I knew received equity top-ups every year. This is not the norm for all companies, though: I know several places that either do not have this in place or only the top 20% might receive any form of additional equity.

Signing cash bonuses are sometimes awarded together with equity, especially when your equity vesting is back-heavy.

For example, the Amazon vesting schedule follows a 5-15-40-40% pattern. You get 5% of your equity the first year, 15% the next, and 40% in years 3 and 4. In practice, this means you get less equity earlier. Amazon balances this out by granting people a cash bonus upfront for years 1 and 2.

Clawbacks are a term where you need to pay back money or benefits if you leave within a certain amount of time. They are most often used for upfront cash bonuses, like the one with Amazon. They might also be used for relocation expenses.

For equity, clawbacks are not needed, as if you leave early, you won't get the equity that you have not vested. However, for vested equity: this should now belong to you, and - in the case of options - you should be able to exercise them.

Post termination exercise window refers to what happens to your vested, but not yet exercised stock when you leave the company - either through your own will, or because you have been let go. If a startup has gone through high growth, exercising the stock options might be very expensive: not because of the price, but because you need to pay tax. This could amount to tens, hundreds, or even millions of dollars.

Many US startups offer a standard, 90-day exercise window. When early GitHub engineer Zach Holman was fired from the company, he had millions of paper gains, but not the money to pay off taxes when exercising. He wrote the Fuck Your 90 Day Exercise Window article that explains why such short windows are a bad deal for employees.

Look for companies that offer 10-year exercise windows: something that is becoming more common in the industry, many Y Combinator startups offering this from the get go. See a list of such companies here.

IPO lockup periods are a time frame when you cannot sell shares that you have vested, following an IPO. The standard term is 6 months for most companies. For example, when Uber went IPO in April 2019, employees could not sell the stock until December 2019. Note that the employer might sell RSUs during this time period to cover taxes for employees.

Typical terms in Big Tech and sensible startup equity are these:

- One-year cliff for vesting for private companies. No cliff for publicly traded companies.

- 4-year vesting of grants with monthly or quarterly vesting. Any longer vesting goes against the usual "up to four years tour of duty" that most innovative companies and organizations utilize - and which "tour of duty" can be extended a few years in, with another, sizable equity grant.

- Clawback on upfront cash bonuses or relocation expenses for up to two years.

- Equity refreshers are variable. Better companies award them to most employees as part of the bonus process. Places like Amazon award them to a small population. Refreshers often have 3-year vesting.

Red flags for equity are - unfortunately - not uncommon. If you spot any of these, proceed with caution.

- Predatory vesting or clawback terms. A few people mentioned seeing clawback clauses on equity where you would need to repay all equity if you left before 4 years.

- Longer vesting period than 4 years: this is outside what is "normal" in tech or a productive "tour of duty". A 4-year vesting is the standard for most tech companies. In Europe, 5-year terms used to be the "norm" up to a few years ago, but this is changing to 4 years for all "reasonable" companies. Anything longer is a red flag - I know of some EU startups offering 6-year vesting periods who get turned down by candidates knowing what reasonable vesting windows are.

- Short windows to exercise options after leaving the company (post termination exercise windows). Many companies have 90-day windows for exercising options. This can be problematic for many people. Look for companies that have 10-year exercise windows - here's a list of such companies. Amplitude was one of the first companies to introduce this setup, and they have open-sourced their approach.

- Stock granted as dollars in a high-growth pre-IPO company can be a yellow flag. In October 2020, Stripe has changed from giving four-year RSU grant to giving out a fixed dollar amount of stock at the end of every year, at the same value. Because most people expect Stripe's stock price to keep going up, this practice means employees will lose out on all stock gains for 4 years. From an employee perspective, they are not getting equity, but a large cash bonus that has no upside - or downside.

In general, seek expert advice to review the equity terms to avoid surprises later down the road. If you could gain enough money to pay for a house from an equity package - you should probably spend comparable time and money on due diligence than you would with buying a house.

3. Stock Options, NSOs and ESOPs

Employee Stock Options (ESOPs) or Non-Qualifies Stock Options (NSOs) are often just called stock options. Options are a common type of equity to be granted by startups and high-growth companies to employees. It's the most common form of equity compensation for companies that are not yet close to an IPO - and, usually, the least understood by engineers.

The option is an opportunity to buy a share of the company ("exercise") at a given price ("strike price") after the option vests.

"How much is my options package worth - both now and in the future, assuming the company goes public/is acquired at $X valuation" is the question you'll want to answer whenever you get an offer with equities. Unfortunately, not all companies make this easy. To do so, you'll need to figure out:

- What ownership % the options would mean if you exercised them. This is relevant typically for pre-seed, seed and (sometimes) Series A companies.

- The option strike price and the fair share valuation that investors paid for in the last round of funding. This is typically information based on the 409a valuation. In the US, the strike price needs to match the 409a valuation at the time. For example, say you are issued 10,000 options at a $10 strike price, which is the 409a valuation at the time. If, at a later point, that company would have an exit at a $50 stock price - may this be an IPO or an acquisition - then your package could be worth $400,000: 10,000 x ($50-10). However, if the exit would be at a $9 share price, your options would be under water, and be worth nothing.

- The price for preferred stocks that investors paid for in the last round. As RevenueCat cofounder Miguel Carranza shares: "you might want to know how much investors paid for a preferred stock in the last round (which would typically have a markup.)"

- Expected company growth that is realistic/conservative / optimistic from your perspective. Future growth is both the biggest opportunity for your equity package to grow in value: but it's equally the biggest risk.

- Expected dilution as the company grows. The company raising money at double the valuation will most likely mean your options/shares will be worth less than twice their current value due to dilution. Dilution can be hard to predict

- Exit scenarios. Options are only worth anything if there will be a financial event - IPO or acquisition - where the shares will become liquid. IPOs are typically a lot cleaner from a financial perspective than acquisitions, where ratchet clauses will protect early investors' interests. See cautionary examples for examples where employees were left with little to nothing after company acquisitions.

- Post-termination exercise period: if you leave the company, how long do you have to exercise options that you've vested? Look for places where this is years, not 90 days. See a list of startups with extended exercise windows here.

Equity issued in different stages of venture funding is hard to compare: it's like comparing apples to oranges. This is because of the expected growth of the company is higher, the earlier the stage. However, the time for any exit is also much longer and more uncertain if it will ever happen, the earlier the stage. For example, most seed-stage, venture funded companies optimistically hope to grow 100x or more, over the next many years. At Series D, E, or F, this optimistic growth is more expected to be 2-5x before a potential exit.

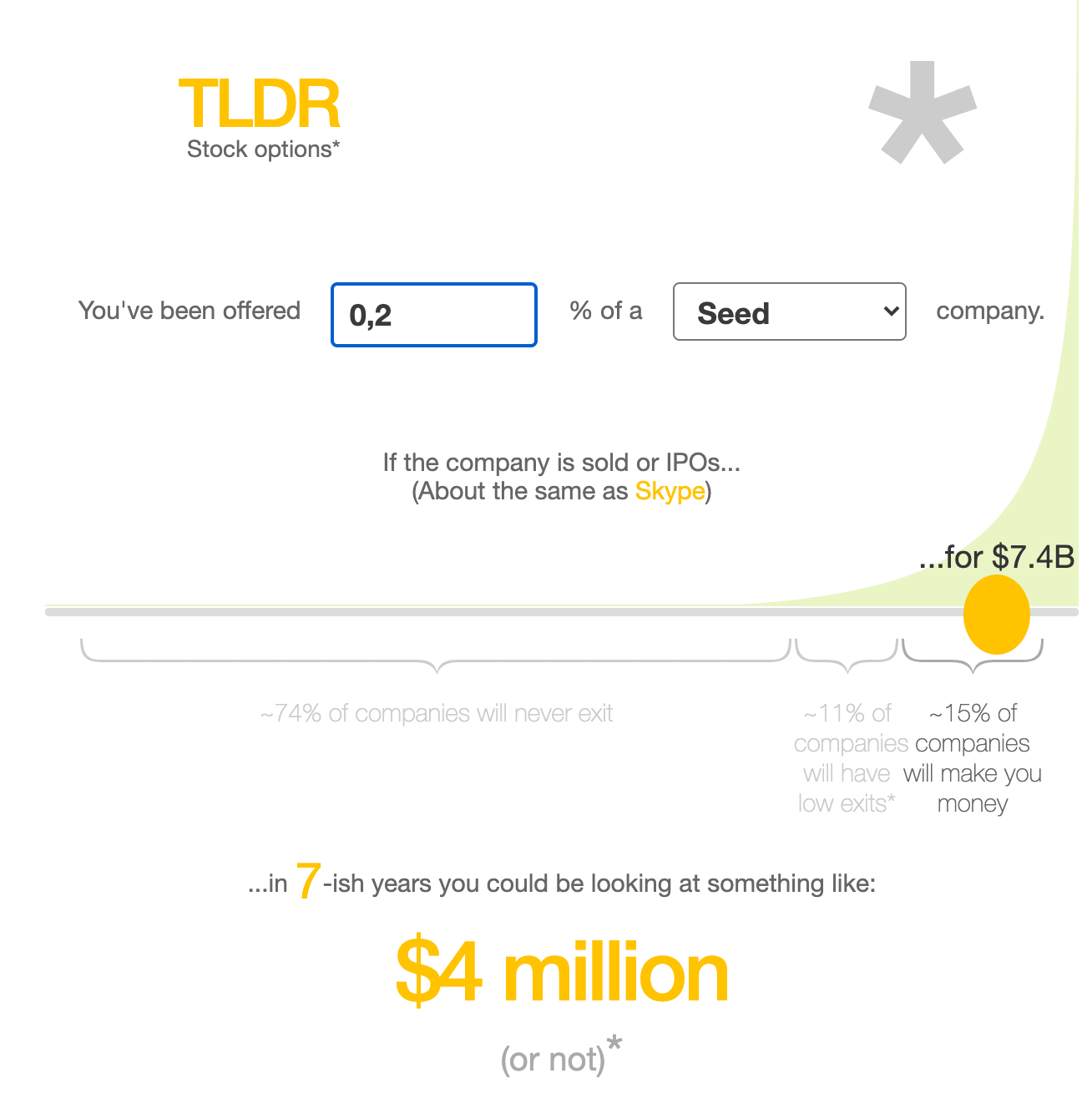

However, the earlier stage the company, the higher risk that they will never exit. Do your research on the industry, the founding team, the investors so you can "price" the value of equity, and the value of a potential outcome. TLDR Options is a site that helps you visualize various outcomes with crude estimations.

Most companies will represent options to be worth more than they probably are, and there's not much you can do about this. As software engineer Dan Luu puts it in this article, "startups prefer options because their lack of value is less obvious than it would be with cash".

Using your own savings to exercise options is the biggest downside of options from an employee's perspective. Let's imagine you joined Uber early on, and you've received 50,000 options at a $4 strike price each. Let's assume that these shares would be valued internally at $44 each in 2017. However, Uber is not public, and you want to leave the company, and let's assume you have a 90-day post-termination exercise period.

On paper, you have made $40 profit on each option and gained $2,000,000 in value. However, you would need to pay $200,000 from your own savings just to exercise these options - and we've not even talked about taxes.

It might be tempting to borrow the money: but what happens if Uber never goes public? You will have lost all that money. What happens if they do go public and you have left and lost the right to exercise those options? You could have left millions on the table. This is yet another reason to look for places that have multi-year post-termination exercise periods.

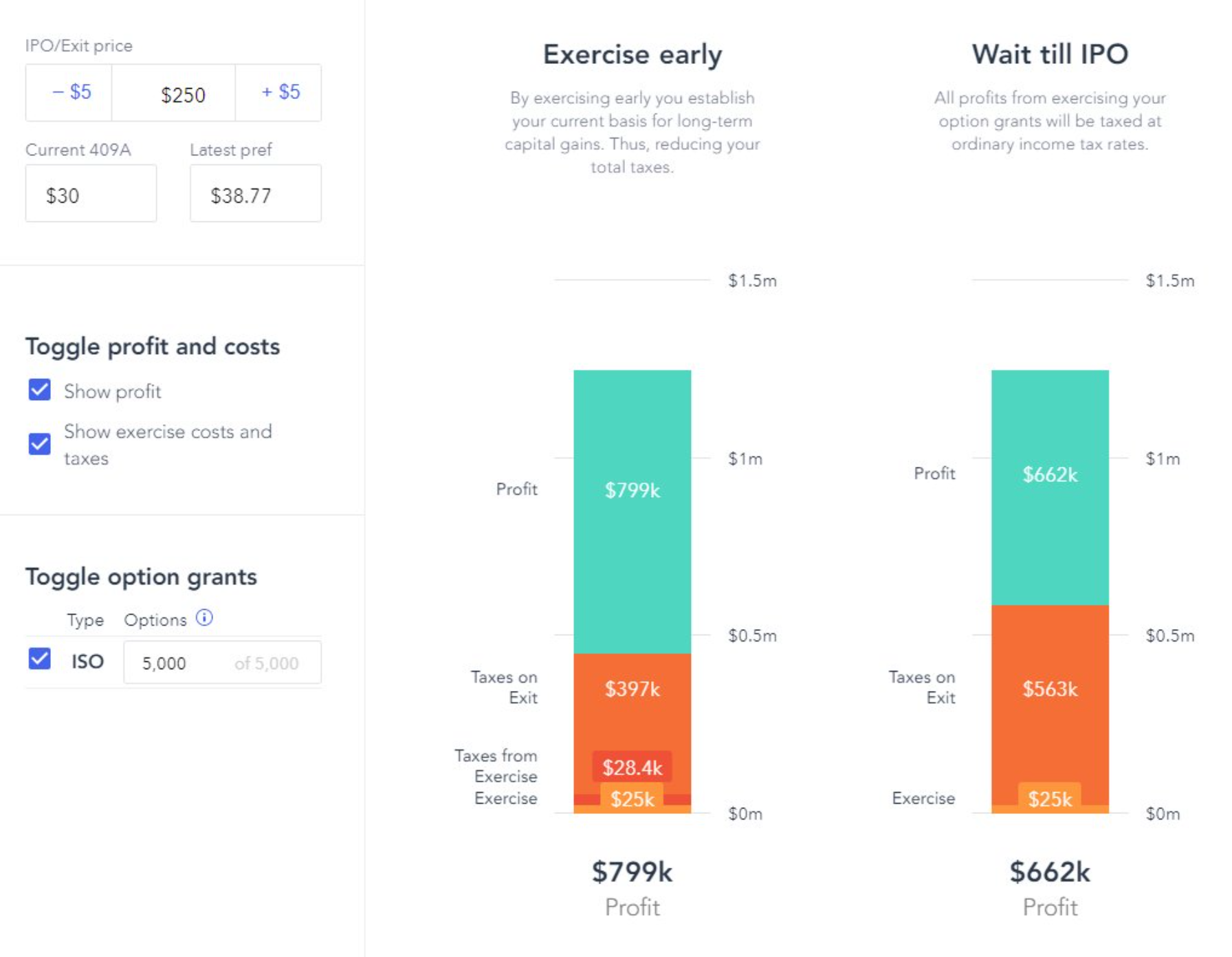

Exercising options early is the number one concept most people in tech mentioned as something they wished they knew about. Exercising options before they vest, can qualify for favorable tax treatment. Here's a case studyof what it would have meant for an early Snowflake employee, instead of waiting for the IPO:

Not having the funds to cover exercising options and the tax is the main reason many engineers shy away from this option. This is where financing solutions providers might help: they can offer no-downside funds to exercise, and then take a fair cut at the IPO, often resulting in more profit than if you would have exercised options later.

Examples of providers who can offer financing solutions include Secfi, Quid, EquityBee, Forge Global. Find others by searching for "stock option financing".

Getting issued options at late-stage companies can be risky, as they might turn out worthless after an IPO, if the company's valuation does not grow fast enough. This is called the options being under water. This is why companies above the $1B valuation typically issue RSUs or double-trigger RSUs.

At Uber, some of the options ended up under water. Some people who joined in 2015 received options at the strike price of around $31 per share. Uber later went public at a $45 value. However, after the lockup expired, the share was at $30. This meant that those options were under water and worthless.

Compare this with employees who joined in 2016, and received double-trigger RSUs. Even though the issue price of the RSU was $48, at a $30 stock price they were still worth 62% of the issue price.

Get professional help in understanding how to maximize your equity value: both from experts like Secfi, and startup equity and tax advisors.

Further reading:

- Options vs cash from software engineer Dan Luu - a must-read for software engineers

- Understanding startup options from YCombinator

- The State of Stock Options in 2020 from Secfi

- Stock Options chapter in the Holloway Guide to Equity Compensation

- Employee Stock Ownership Plan (ESOP) on Investopedia

- Exercising stock options from Carta

- Fuck your 90 day exercise window from an Zach Holman, an early GitHub engineer

- List of startups with extended exercise windows that are longer than 90 days

- Secfi: a company to help make the most of your stock options

4. RSUs (Restricted Stock Units)

Publicly traded companies are on the stock market - like Microsoft, Google, Amazon. Anyone can buy and sell their stock after opening a stock account.

RSUs - Restricted Stock Units - are a form of stock compensation that publicly traded companies often offer to software engineers. You'd typically get awarded a specific amount of stock that vests over a given time period.

Depending on the terms of the stock, it could be awarded in various ways:

- You get awarded a number of shares: converted from the dollar amount from when your award is approved. Say you get awarded $120,500 in Microsoft stock that vests over 4 years. Let's assume your stocks get awarded when the Microsoft stock price is $241. You would get awarded 500 units that vest over these 4 years: or 125 units per year. If the price of Microsoft stock goes up or down, so does the value of this package. Once the stocks vests, you can decide to sell them or keep holding them.

- You get awarded a dollar value of shares that get converted to shares on vesting. Say you get awarded the same $120,500 in stocks to vest over 4 years. Regardless of the stock performance, you'd receive $30,125 per year in stocks. Once you get these stocks, you can sell or keep holding them.

Companies have an RSU policy. However, most places would award a number of shares at the start of your vesting period, making you more of an "owner" and someone who can benefit more from the stock price going up.

Further reading:

- Restricted stock on Wikipedia

- What is Restricted stock? on Investopedia

- Restricted Stock Unit section in the Holloway Guide to Equity Compensation

5. Double-Trigger RSUs

Pre-IPO companies are private companies that are not listed on any stock exchange. Only private investors investing in the company can buy shares, usually as a form of an investment rounds.

Double-trigger RSUs is a concept more common for unicorn companies that plan to go public in the coming years. These companies allocate stock to employees that vests similar to how RSUs do with public companies.

The problem with awarding RSUs for private companies is taxes. You'd need to pay tax the income from the stock value that you've vested: however, there is no market to liquidate this stock. You'd have to pay out of pocket for the tax, with no way to sell part of your equity cover those taxes.

Double trigger RSUs is a setup Facebook utilized before its IPO, and several other companies have followed since. The idea is that the stock does not vest until a second trigger - an IPO or another financial event happens. This way, taxes are due on the IPO or company sale, but not before.

Further reading:

- Pre-IPO tech giants use Double-Trigger RSU vesting to attract talent

- Private company stock grants plan design trends

6. ESPP (Employee Stock Purchase Plans)

Employee Stock Purchase Plans (ESPP) is a benefit offered mostly by publicly traded companies. It allows employees to buy stock 5-15% below the fair market value.

Details of ESPP can seem complex, but it's worth understanding, as you can benefit from participating.

- Enrolment period is the time you need to decide upfront how much of your salary you contribute.

- ESPP lookback provision is a key part of ESPPs. You will purchase stock at the lower or either the offering date or the purchase date share price. Basically, if the stock rises significantly during the period, you might be able to purchase the stock with far more than a 15% discount. See an example here.

- Contribution limits curb how much of your salary you can contribute. ESPP is typically a solid deal, and the limits ensure you can't benefit too much from enrolling.

I benefitted quite a bit from ESPPs both at Microsoft and at Uber. Both companies had a generous program with offers to buy stock 15% below the fair market value and contribution limits of about $20,000 per year.

Further reading:

- The untold advantages of your employee stock purchase plan

- ESPP on Investopedia

- A good ESPP is a no-brainer

- Have an ESPP? Beware of the risks.

- Is ESPP a risk free investment? from the Money Stackexchange forum

7. Phantom Shares

Phantom shares or shadow stocks are similar to awarding RSUs - but without actually giving out any company stock. Employees receive "mock stock". The stock follows the company's stock price changes, and pays out profits after vesting. Profits might mean the difference in share price since issuing, or the price of shares on vesting.

- Appreciation only plans would only pay the "profits" of the stock increase, since the phantom stock was issued. Say you got awarded one phantom stock when the company's share price is $100. By the time the share vests, the company share price is $150. You would be paid out $50 in cash.

- Full-value plans would pay out the full stock value on vesting. Taking the previous example, you'd be paid out $150 in cash when the vesting period ends.

Phantom stocks are uncommon for Big Tech, but a few tech companies in the EU issue them. Adyen - a competitor to Stripe - is an example of a company who grants phantom shares to its employees.

Further reading:

- Phantom stock plan on Investopedia

- 9 frequently asked questions about phantom stock plans

- Phantom stock: what is it?

- Why phantom stock can be better than real stock

- Less common types of equity: phantom stock from the Holloway Guide to Equity Compensation

8. SARs (Stock Appreciation Rights)

Stock Appreciation Rights (SAR) are an interesting middle-ground between stock options and RSUs and are probably the most similar to phantom stocks.

Employees would gain the increase in the stock price of the company, during a pre-defined period. They are almost always paid out in cash. They are sometimes issued parallel with options as tandem SARs, so the gain in SARs will help with buying the stock options.

SARs are not a type of equity you'll see with US tech startups. You might come across them with some startups preferring this setup in the EU. There are both advantages and disadvantages of SARs both from an employee, and a company perspective.

As an employee, SARs could be seen as more beneficial than options, the biggest benefit being how you don't have to pay upfront to exercise them. You basically get cash for the value increase - the payout usually tied to a company liquidity event that happens while you work there.

The main drawbacks are how, as an employee you have little flexiblity to choose when to exercise after vesting occurs. Also, unlike stock options you exercise, with SARs you typically won't have ownership in the company after you leave - and you might be left with less if, say, an IPO occurs a year after you left.

Further reading:

- Stock appreciation rights on Investopedia

- Difference between ESOPs & SARs on MyStartupEquity blog

- Pros and cons of SARs and stock options

- Incentivising employees in start-ups through SARs

- Less common types of equity: stock appreciation rights from the Holloway Guide to Equity Compensation

9. Virtual Shares, Virtual Options

Virtual shares are a synonym to phantom shares, and are increasingly adopted by European startups. They are similar to RSUs, except they only trigger a financial event - and thus "vest" - when the company experiences a financial event (e.g. is acquired or goes public).

Virtual share plans are becoming popular in countries like Hungary where setting up options or regular share plans would carry much more administration, and tax burdens for employees.

Virtual options are designed similarly to avoid taxation until a financial event happens. This setup removes risks of employees losing their capital if the company either does not have a financial exit, or the exit would be below the option's strike price.

Both virtual shares and virtual options are contracts you need to carefully design. When done well, they can greatly benefit employees, and help companies attract more talent, without the downside of employees having to risk their capital for an uncertain exit.

Further reading:

- Virtual share plans: the right tool for Hungarian startups to attract and keep talent on Financier Worldwide

- Startups and virtual options from a corporate law firm Raue

10. Growth Shares

Growth shares are a setup where you can get shares only after the company has grown in some way. You are issued the shares only after a "hurdle rate" has been met: which typically correlates to business results improving for the company.

Growth shares are usually far less advantageous for employees than other types of shares. When I joined Skyscanner, I was offered growth shares that would have been worth nothing until the business grew by 20%: so it was like an "underwater option".

Similary, following massive growth, Revolut changed to issung growth shares. An employee shared to Sifted:

“Revolut used to be amazing for equity, but now they offer growth shares, which are useless”.

Growth shares are advantageous for the business as they only have to pay if the business grows. They are shares offered mostly by EU startups, Skyscanner and Revolut being good examples on this.

Further reading:

- Growth shares overview

- Revolut issuing growth shares with a pricey hurdle rate

- Growth shares share schemes

- What are growth shares?

11. Dilution

You joined a startup when it was valued at $100M and received options that you calculated to be worth $100,000 over four years. Four years later, the company is worth 20x that, at $2B. Is your equity also worth 20x that, or about $2M?

Doubtful.

It's probably worth less than that. It could be worth 5x, 10x, or even 15x: all depending on dilution.

Dilution occurs when a company raises new investment, and the new investors receive freshly issued stock at the expense of existing stock holders - founders, earlier investors, and employee stock holders. For high-growth companies who raise several funding rounds, some level of dilution will be an ongoing characteristic.

Startups growing at a healthy pace will see stock holders own a smaller piece of a larger pie - but the pie growing typically offsets the shrinking in ownership.

At the same time, dilution is rarely the cause for employee stock options not being worth much. Not getting to a liquidity event or just stopping to grow are far more common cases. And remember: there is nothing you'll be able to do about dilution as an employee. However, you might be able to impact growth: and very high growth with high dilution almost always has better outcomes than slow growth with little dilution.

Further reading:

- Dilution: the good, the bad and the ugly from TechCrunch

- The dangers of share dilution from Investopedia

- Equity dilution for early stage startups from Silicon Valley Bank

12. Taxes

Regardless of what type of equity you'll be issued, taxes will be a key question. When are they due? What is a sensible strategy to optimize them? What options do you have to change how your gains - or losses - are taxed?

Taxes on top of exercising options are often a huge surprise factor, especially for late-stage unicorn employees. Secfi collected data from individuals in more than 700 late-stage unicorn companies in the US and found taxes to account for more than 6x the exercise price in this study:

Taxes are outside the scope of this article beyond the fact that they will be due. Especially with options and non-liquid stock, they might be due before you can realize the value of your equity.

Do your homework and talk to accountants to understand the tax implications. Decide if you want to exercise early - and if you don't have the funds to exercise and pay taxes, look into financing options like Secfi who might help out. Here's a case study of how early exercising Snowflake options over waiting for the IPO would have saved $130K for an engineer - or 20% of their stocks.

The greater your gains, the greater your tax bill could be: be prepared.

13. Why Equity is Illusive: Cautionary Examples

While employee stock is generally something positive, there are plenty of ways you can see no money from them: and even lose money on the stock.

Equity being worth less than what you banked on is a very common case with publicly traded companies and Big Tech. The simplest case is joining a publicly-traded company at a time when its equity value is slowly going down. For example, if you would have joined Snap in 2017, issued an equity grant of $200K/year at the $20/share part, by 2019 the stock would have been down at $5/share, taking this grant to $50K/year.

At larger companies, equity "top-ups" might have made the "decrease" less painful. And just as stock can go down, it can go up: Snap is trading at $61 - 3x of the $20 price range - as of February 2021.

Equity being worth nothing is the most common outcome with startups. The company might never go public. It might be sold at a price where common stock - and options - are worth nothing thanks to ratchet causes protecting the early investors. The company might never have a financial event.

If you joined the "next and better Uber", you'd have gotten nothing. Sidecar was the first "true" ridesharing company, connecting riders with drivers who did not have to be black car drivers. Still, despite innovating ahead, the company shut down a few years later. Anyone with equity in the company was left with nothing.

As another story, one of my friends worked at five startups, over five years, exercising options in each. Only one of the startups ever had an exit: it got sold to another company. My friend had stock worth around $50,000 on paper when he left. He received $215 as proceeds from the sale.

Company valuations collapsing like WeWork did and employees losing big money is not as uncommon as it seems.

WeWork was on track for a $47B IPO in 2019, which would have made many employees millionaires. However, this all collapsed in a matter of 6 weeks. Instead of the IPO, Softbank took control of WeWork. Some employees "only" lost hundreds of thousands of unrealized gains. However, the 500 to 1,000 early employees lost hundreds of thousands that they paid on their tax bills when each share was valued at $50 - and which share price was now reduced to $4.

Employees losing big money by exercising options is not a common story, but one that has happened several times - and not just to WeWork early employees.

Good Technology was valued at $1B in 2014 and planned to go public. However, in 2015 Blackberry announced it would acquire Good Technology for $425M in a fire sale. Several employees lost large amounts of savings as they paid cash to exercise options, bought stock in the company, or paid taxes on the common stock they received.

The takeaway from this story is that company share prices can go down as much as up, and when a company is sold, common shareholders might end up nearly empty-handed.

Fast-growing companies needing to lay off staff and slash company valuation - and thus, the value of any equity also happens frequently. By nature, high-growth is tied to high risk, and sometimes that risk does not pay off. There's a fair chance you could be laid off during this time. Even if you are not, your equity value is unlikely to be worth as much as it did before.

Zenefits went from a $4.5B valuation to laying off 45% of people in less than two years in 2017. Bird laid off a third of employees when COVID hit, and demand for scooters dried up overnight.

When companies are acquired by private equity, existing shareholders might see little value for their stock, even if the company is later sold or taken public.

FanDuel was a seemingly rocketing unicorn, where founders and several employees were millionaires on paper. However, after a failed merger with competitor DraftKings, bookmaker Paddy Power Betfair acquired FanDuel for $465 million. As part of the sale, founders and employees got nothing. Lawsuits are still in progress, but employees are likely to see nothing of the sale.

The case of the convertible note not converting is a rare and interesting story. Toptal employees were promised stock, but even the company's co-founder was empty-handed. This was because all stakeholders received a convertible note that granted them equity if and only if Toptal raised more money in the future, after their seed round.

In almost all cases, companies raise more money. TopTal never did, and thus the founder still owes 100% of the company stock. Lawsuits are in progress, but employees will likely never see stock.

Further reading:

- WeWork staff planned their life around a stock deal that collapsed

- Zenefits went from a $4.5B valuation to massive layoffs in less than two years

- Good Technology wasn't so good for its employees

- Good Technology's $425M fire sale to Blackberry

- FanDuel founders spin juicy tale in suit against investors. The funds have a different story

- FanDuel founders and employees file lawsuit against investors who cheated them

- When a unicorn startup stumbles, its employees get hurt

But How Do You Get Into These Companies?

Most engineering positions still don't offer any equity: Big Tech and high-growth startups who want to recruit exceptional talent are the ones who typically do.

I don't have all the answers, but I do have plenty of experience both interviewing for these companies, and helping others prepare for interviews.

If you're interested in interview preparation advice for senior and above engineers and engineering managers, subscribe to these (free) emails from me here. I won't publish the contents on this blog - they are my raw thoughts, and I'd ask you to not share them elsewhere.

Subscribe to my weekly newsletter to get articles like this in your inbox. It's a pretty good read - and the #1 software engineering newsletter on Substack.