The Collapse of Silicon Valley Bank

👋 Hi, this is Gergely with a bonus issue of the Pragmatic Engineer Newsletter. In every issue, I cover challenges and events at Big Tech and high-growth startups. To get full newsletters twice a week, subscribe here.

It’s been a wild weekend, starting Friday. In case you somehow missed it: we went through the fastest bank run in history, in an event that impacted about half of all VC-funded startups in the US and UK. On Friday night, Silicon Valley Bank (SVB) was shut down by regulators, triggering a weekend of fear and uncertainty for many people and businesses with questions like: “can we make payroll next week?” There was no certainty for startups with money in Silicon Valley Bank.

As of today (Monday) things have calmed down, but it’s not all over. In this special edition, I cover the events of this blow to the tech economy.

Half of all venture-backed companies in the US used SVB, making the bank the most important financial institution in the US startup tech sector. It wasn’t just startups, but also late-stage companies: 44% of venture-backed tech and healthcare companies which went public in 2022 were SVB customers, according to Bloomberg.

Thursday: Bank run

On Thursday, 9 March, we witnessed the fastest bank run on record.

What is a bank run?

This is when customers show up at a bank to withdraw all their money, due to lack of confidence that their funds are safe. The issue is that banks (not only SVB) aren’t designed to work like this: they cannot fulfil simultaneous requests for withdrawals by all (or even most) customers. Basically, a bank doesn’t have everyone’s money easily to hand, locked up in a vault. This is because when you make a deposit with a bank, it uses some of your money for a variety of purposes:

- Loans to other customers as credit

- Short-term and long-term investments

- Some is free-floating, available to customers

If a large percentage of customers suddenly want their money, a bank can do this to the extent that their free cash flow allows. Beyond that, longer-term investments need to be unwound: potentially breaking up long-term bonds that they bought, or their selling of debt they hold to other institutions. Breaking up or selling off any long-term investments may come at a loss, and there’s a danger the bank may still not have clawed back all customer deposits, meaning some could lose money.

In a bank run, only those who act first secure their funds. Those moving later might not get all their funds and could even lose some of their holdings. This is why even talk about bank runs can be hazardous: if you hear a bank run is starting, the rational move is to minimize your losses by getting your money out, which helps make the run a reality.

Bank run at SVP

Thursday, 9 March, Around 9am in the morning (PST / California time), founders were tipped off by venture capitalists that SVB looked in trouble. The investors suggested companies immediately withdraw their funds for safekeeping, while still possible. From here, things accelerated.

11am: Bloomberg reported that Founders Fund, a VC fund co-founded by Peter Thiel, advised all its portfolio companies “to pull money from Silicon Valley Bank.” This news is widely shared on social media and in private messages.

11:30am: SVB CEO, Gregory Becker, holds a 10-minute conference call with top VCs, saying the bank has “ample liquidity to support our clients with one exception: If everyone is telling each other SVB is in trouble, that would be a challenge.” According to The Information, the CEO said:

“I would ask everyone to stay calm and to support us, just like we supported you during the challenging times”

12pm (noon): Details of the call leak, and focus shifts onto the CEO’s quote: “If everyone is telling each other SVB is in trouble, that would be a challenge.” On social media, founders share that they are observing a bank run to be unfolding. This news naturally fuels the run.

OK i am hearing from dozens of founders about what to do at SVB.

— Howard Lerman (@howard) March 9, 2023

It's an all out bank run.

From 12am: VCs tell portfolio companies to pull money they have in Silicon Valley Bank. The bank’s systems start to be overloaded to the point of customers not being able to log on and transfer.

We were witnessing a full-on bank run unfold in a matter of hours, bank customers transferring out all their holdings.

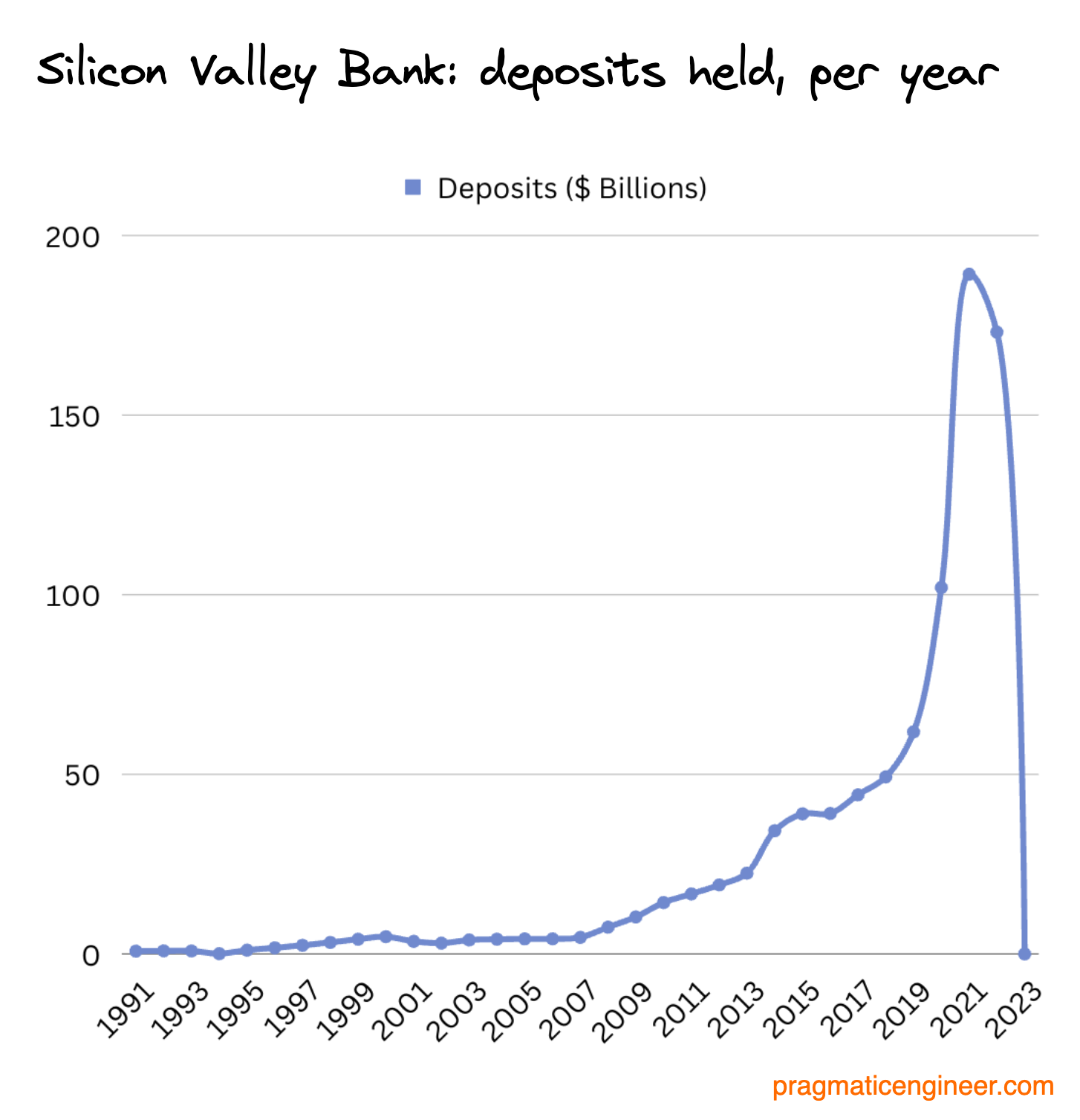

In the aftermath, we would learn that Silicon Valley Bank processed $42B in deposit outflows on Thursday: which is nearly a quarter of all deposits they held!

Here’s a first-hand account of how things went for one customer, Alexander Torrenegra, founder of Torre.co, a platform to find work or be found.

“Thursday, 9 AM: in one chat with 200+ tech founders (most in the Bay Area,) questions about SVB start to show up.

10 AM: some suggest getting the money out of SVB for safety. Only upside. No downside.

10:50 AM: I read the messages in a bathroom break. Immediately cancel the meeting I had. Ask my wife, Tania, to wire all of our personal money out to other banks. Call my teams. Ask them to do the same. One of them, at the dentist, has to stop the procedure and run home. (...)

~12:00 PM: All of my chats with tech founders in the US light on fire with what’s happening. Obviously, we have a bank runoff. Surreal.

12:30 AM: We request two wires for all the money from the 2nd company to Mercury.

12:38 PM: Wires to Ameritrade clear. The 1st company is safe. (...)

~3:00 PM: My chats with tech founders from Latin America start to catch up.

4:05 PM: SVB calls us. Tells us that our savings will be wired the same day, as requested.”

Friday: Downfall of SVB

On Thursday afternoon, several startup founders I know got the memo to move their money, but they couldn’t log into SVB and do transfers. Most planned to transfer funds out the first thing Monday morning. Some founders even showed up at the offices of Silicon Valley Bank in San Francisco. As fellow Substack author Eric Newcomer reported:

“Founder Dor Levi, a former Lyft executive, first texted me at 8:16 a.m. from outside Silicon Valley Bank’s New York offices.

He said he’d been instructed by a banker at Silicon Valley Bank to go and get a cashier’s check from the New York office if he wanted to move his funds.

Levi wasn’t the only founder who showed up at SVB’s offices looking to pull his money from the bank. “There’s more founders coming every minute,” Levi texted. He said about a dozen founders showed up at the bank this morning.”

The founders showing up at the bank in person couldn’t withdraw their money. In fact, no one could.

On Friday morning, the Federal Deposit Insurance Corporation (FDIC,) announced it was closing the bank. The FDIC is a government agency whose goal is to maintain stability and public confidence in the US financial system.

The FDIC stated “all insured depositors will have full access to their insured deposits no later than Monday morning, March 13, 2023.” This meant companies had guaranteed access to $250K on their account, but everything else was uncertain.

This was bad news and the implications were just starting to become clear.

Saturday: Reactions and preparing for bad outcomes

By Friday midday, it was less than 24 hours since SVB was the largest startup bank, to a state of collapse. Customers not quick or lucky enough to transfer their money out had their accounts frozen for all of Friday, and could only hope to access $250K in deposits. This may sound like a lot for a personal account, but for a company with 30 employees on $150K each and monthly AWS costs of $100K, it would barely cover 2 weeks of wages and infra costs.

As a result, making payroll was looking like a huge problem for many companies. For tech startups, the biggest expenses tend to be:

- Staff payroll

- Infrastructure and vendor costs

There’s a good reason why these same tech companies have been doing layoffs and aggressively cutting back on vendor spend: it’s because staff payroll and infra vendor costs are the bulk of their expenses. In the US, payroll is every two weeks and most startups had a payroll cycle starting this week (the week of 13th March) In contrast, in the EU payroll is typically monthly.

I talked with a well-connected founder, who said::

“My WhatsApp is insane with SVB. 4 founders I know won’t make payroll unless they can bridge somehow. They are literally asking me for personal loans.

My inbox is a bloodbath.”

Garry Tan, CEO of Y Combinator stated how “30% of YC companies exposed through SVB can’t make payroll in the next 30 days.”

Given payroll was the immediate priority, founders for whom $250K wouldn’t cover the payroll jumped into action, reaching out to VCs for bridge loans, and asking friends and family to loan enough so they could pay staff.

Employee-of-record (EOR) payroll companies such as Remote, Deel, Rippling found themselves in a challenging situation. These companies are hired by startups to manage payroll in countries where a startup is not a legal entity.

Rippling, a popular payroll provider which also provides payroll, was immediately impacted because it used SVB to transfer salaries. When SVB went down, Rippling could no longer make these payments, so it rapidly switched over to JPMorgan Chase to make payroll, but warned customers that payroll might be late as a result.

Meanwhile, other EOR providers have assured customers that their staff will get paid, even if customers won’t be able to transfer payroll the next week. On Saturday, Remote confirmed it was still making payroll - even if customers cannot transfer funds - and on Sunday Deel announced it will support impacted customers.

EOR providers are in a tight spot themselves, as legally they cannot fail to pay employees in some countries, due to employment law. At the same time, with so many customers having had their accounts frozen, these providers could potentially have liquidity issues, meaning EORs could have had problems making payroll.)

Vendor payments for the coming week were looking to be at risk by Friday. For any startup with funds stuck in SVB, they had to budget the $250K they could access, and do so wisely.

Other vendor expenses were arguably secondary until startups could access their full account, so founders were debating asking vendors to defer payments, given the unprecedented situation.

Several vendors were proactive, offering payment support. On Friday, project management app Linear announced it would grant payment delays. On Saturday, error logging service Sentry followed suit, and PaaS Vercel did the same.

For some startups, losing access to their bank account prompted drastic action. While startups with relatively small expenses hoped to ride out the coming weeks on the insured $250K: for larger companies with all their funds tied up, this wasn’t an option.

One example of this is Camp.com, a company selling themed toys for all ages. Responding to its bank account being frozen, the startup launched a site-wide 40% off sale, with this popup displaying to all visitors:

A 40% discount is huge for a store like Camp, which sells physical goods. A site-wide 40% most likely means the company was selling everything at a loss, in a desperate bid to generate cash flow and continue operations while the bank account was inaccessible.

The campaign and the cheesy graphic worked: Camp saw 35x the normal traffic, and – presumably – several times the sales.

Founders were fearful of a liquidity crunch and the effects it could have. By Saturday, it was understood the FDIC would move swiftly in selling SVB’s assets and aim to return deposits as fast as possible. The question really was: how fast? Was it possible by Monday?

In the early hours of Saturday, a message circulated in VC circles, claiming the FDIC had already sold about half of SVB’s assets, and planned to make 50% of deposits available by Monday, with the other 50% likely to be recovered in 3-6 months.

While this was better news than having access to only $250K, it still forecasted grim news and a liquidity crunch. After all, if 50% of a company’s reserves disappear, it will need to do drastic cost-cutting measures like refusing to pay non-essential vendors, laying off staff, and cutting down on expenses for up to 6 months until the deposits are returned.

Sunday: Containing the crisis

On Sunday afternoon, at around 5pm PST, the US Department of Treasury, the Federal Reserve and FDIC issued a joint statement, stating all depositors were fully protected, and Silicon Valley Bank customers will have access to all of their money starting Monday.

The statement went on to state that no losses associated with the sale of SVB assets would be borne by taxpayers. Only shareholders and certain unsecured debt holders were not protected from this.

In the UK, Silicon Valley Bank’s bankruptcy also caused a similar stir, because its UK entity was also a favored bank among UK startups. UK SVB held deposits of £6.7B ($8B) and served 3,300 clients, likely around half of VC-backed startups in the country, according to Sifted. The UK entity collapsed on Friday as well.

In another positive outcome, HSBC bank announced acquiring SVB UK for the symbolic sum of £1. The acquisition means customers of SVB UK have access to all of their deposits as of Monday.

Both in the US and in the UK, a crisis has been averted by ensuring depositors have access to all their money, which is the outcome financial analysts expected since Friday. On Friday, former Bloomberg columnist

“Let’s talk about the big risk: financial contagion. Many people will undoubtedly have traumatic memories of 2008, when Lehman’s collapse triggered a systemic meltdown. That is a real possibility, and it’s why the FDIC and other government agencies are probably going to work very hard to make sure SVB’s depositors don’t have to take haircuts.

But there are reasons this is not like the Lehman shock. (...) SVB didn’t have enough links to the rest of the financial system to cause a 2008-style cascade, but there could still be a wave of runs from plain old panic. Panic doesn’t need a rational reason, and in a bank run, panic becomes a self-fulfilling prophecy. (...)

In general, I’m optimistic about the system’s ability to contain the fallout from SVB. So far the U.S. economy has powered along with record employment and strong growth, even as the tech sector has gone into a slump. There’s not a lot of reason to think this basic pattern will change after this bank run, and the government has every reason to make sure it doesn’t change.”

Monday (today): Next steps for startups

With the crisis averted, what’s the immediate priority for startups?

Startups are setting up multiple bank accounts. Startups have had a wake-up call about just how risky it is to have all their capital in one bank. Going forward, for startups with sizeable funding – above $1M – it will be a sensible hedge to use at least three bank accounts:

- One main account for expenses, with about 3 months’ of funds.

- One account for emergency funds of ~3 months runway.

- One account to store the majority of funding, with an institution that is diversified: meaning most customers are not startups, in order to avoid the risk of a bank run. Some startups are setting up multiple money market funds to spread their investments.

Every startup I’m in touch with has put together a banking strategy, are busy opening new accounts, and re-distributing funds.

Startups are moving deposits from “startup-first” banks and neobanks. Given no bank can be assumed to be safe from a bank run, startups which previously held most of their deposits in other startup-friendly banks or neobanks are also moving them by opening up secondary or tertiary accounts with some of the largest banks: JPMorgan, UBS, Goldman Sachs in the US and Barclays and HSBC – now the owner of SVB UK.

Startup-friendly banks include Mercury, First Republic, Brex, and Jiko in the US. In Europe, such banks include Mozo, Revolut, Starling and Wise.

So why did so many startups choose SVB as their banking partner? And what is the long-term impact on the tech ecosystem? I answer both questions in this week's full issue on The Pragmatic Engineer, where I additionally cover:

- Why did so many startups use Silicon Valley Bank? The approach SVB had that was different to traditional banks, and services they offered.

- The longer-term impact on the tech ecosystem. Startups building buffers - and cutting costs -, a growing distrust in VCs, tech workers and the risks of startups.

- Why will high interest rates have a longer-lasting impact on startups than the SVB collapse? And could it be that this collapse was a canary in the coal mine – a sign of what’s to come?

Further reading

Since SVB’s collapse unfolded, there’s been plenty of analysis. Here are some articles I found insightful:

- Why was there a run on Silicon Valley Bank? by Noah Smith

- The demise of Silicon Valley Bank by Marc Rubinstein

- The end of Silicon Valley (Bank) by Ben Thompson

- Startup bank had a startup bank run by Matt Levine (Paid)

Subscribe to my weekly newsletter to get articles like this in your inbox. It's a pretty good read - and the #1 software engineering newsletter on Substack.